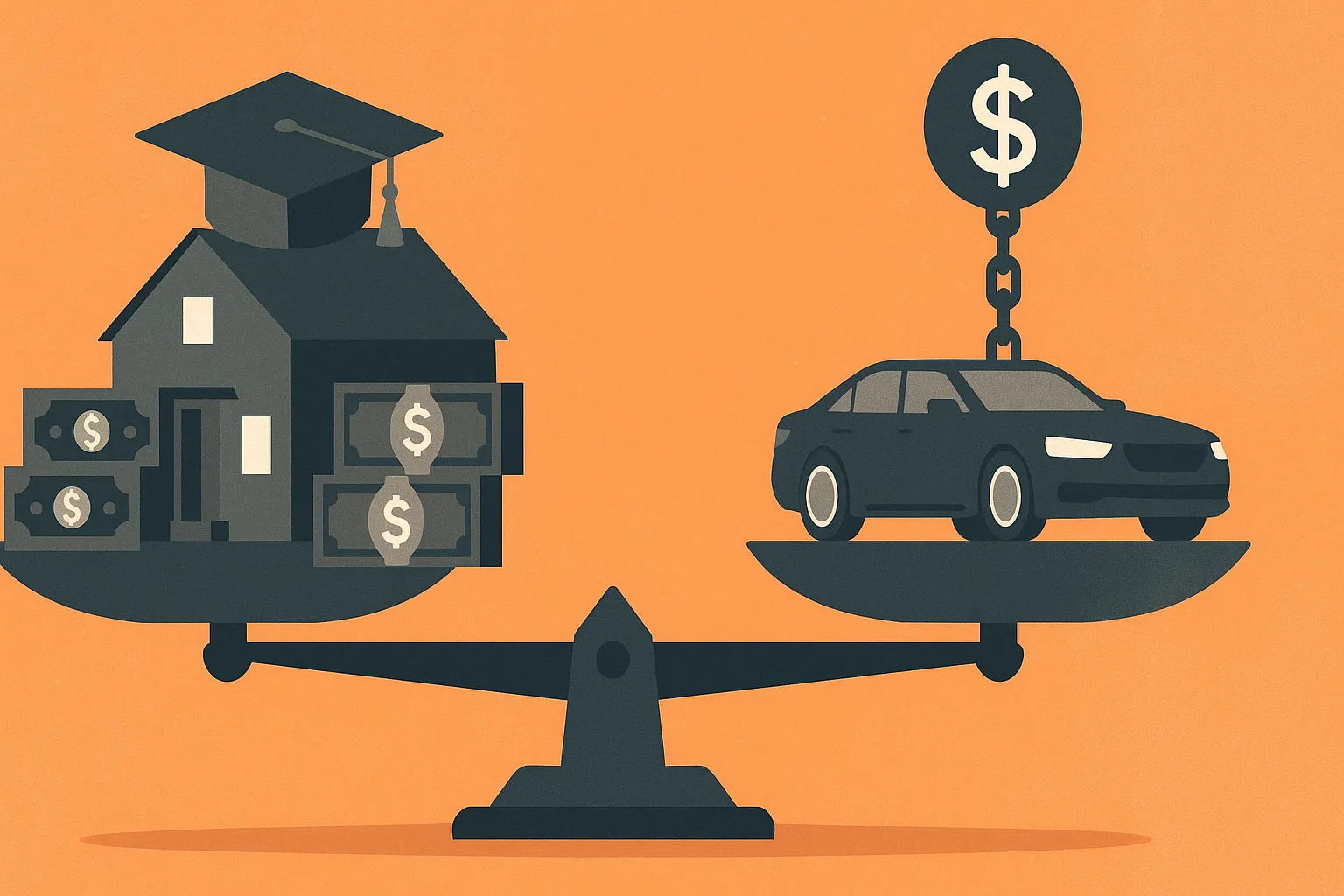

Is All Debt Harmful—or Can Some Support Wealth Building?

As of early 2025, U.S. household debt reached a record $18.2 trillion, according to the Federal Reserve Bank of New York. Yet not all debt plays the same role. Some see any borrowing as a setback, while others recognize that under the right conditions, debt can help build wealth. This article examines when borrowing becomes a strategic asset—and when it becomes a liability.

Key Takeaways

- Some forms of debt—when tied to appreciating assets or income opportunities—can contribute to financial growth.

- High-interest consumer debt, such as credit card balances, typically erodes wealth rather than supports it.

- Debt used for education, real estate, or entrepreneurship may create long-term value if structured properly.

- The biggest risks stem from poor timing, overuse, or misunderstanding of loan terms and tradeoffs.

- Smart borrowing requires clear alignment between debt terms, cash flow, and expected asset performance.

Debt Itself Isn’t the Problem—How It’s Used Is

Blanket anti-debt advice ignores the nuance behind why people borrow. While some debt introduces risk, other types can unlock access to income potential or appreciating assets.

- Hypothetical Example: A person in their late 20s considers a $60,000 graduate degree. Paying upfront would drain savings and limit investment options. Instead, they take out a federal loan at 5%. If the degree increases earning power over time, the decision may create more financial flexibility—not less.

Not all degrees or loans yield strong returns. But in the right context, borrowing can be a means to invest in future capacity.

Why Revolving Credit Usually Works Against You

Credit cards generally fund spending—not assets. They can often support short-term consumption, and carry interest rates few investments can overcome.

By early 2025, average credit card APRs had climbed to 21.37%. At those levels, debt compounds quickly and can spiral without aggressive repayment.

In most scenarios, eliminating high-interest balances should come before investing or taking on new loans.

Mortgages: Common—but Not Always Straightforward

Real estate loans are among the most common forms of debt viewed as “good.” But the details matter.

Mortgages may offer tax benefits and equity growth—but also come with ongoing costs like property tax, maintenance, and insurance. There's also opportunity cost: capital used for a down payment could have been deployed elsewhere.

Still, if the home value increases steadily and fits within a larger financial plan, long-term ownership may prove beneficial. A 30-year fixed loan at 5.5%, when paired with property appreciation and housing utility, may outpace renting over time—especially in high-cost regions.

Business Loans: Leveraging for Entrepreneurial Growth

Borrowing to launch or expand a business can be a strategic decision, particularly when outside capital isn't available.

Small Business Administration (SBA) loans, equipment financing, or lines of credit offer early-stage funding—but repayment schedules are fixed regardless of revenue.

- Hypothetical Example: An entrepreneur borrows $75,000 to open a niche food brand. If demand builds and the business achieves scale within two years, the debt may act as a launchpad. If not, repayment pressure could strain both the business and personal finances.

Debt’s value hinges on execution and adaptability.

Emotional Traps: The Behavioral Side of Borrowing

Debt also carries psychological weight. Anxiety, avoidance, or guilt can lead people to make choices based on emotion—not structure.

Studies show borrowers might often focus on total owed instead of interest rates or repayment strategy. This can lead to prioritizing the wrong balances or deferring action.

Better outcomes may come from:

- Targeting high-interest debt first

- Exploring consolidation options

- Matching payments to income cycles

- Viewing debt as a resource—not a personal flaw

The emotional framing of debt influences how effectively it’s managed.

Borrowing Isn’t a Failure—It’s a Financial Decision

The presence of debt doesn’t necessarily signal poor planning. What matters is the rationale, structure, and fit within a broader strategy.

Debt used intentionally—to grow skills, acquire assets, or fund business creation—can align with long-term resilience.