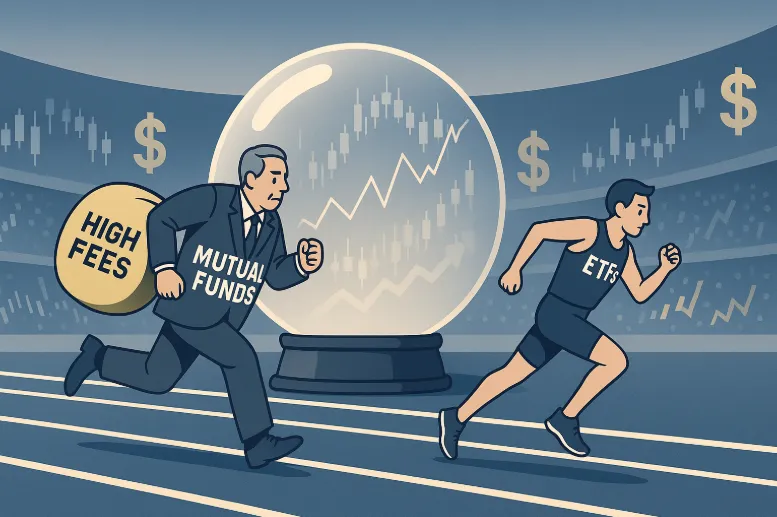

Mutual Funds Are Losing – ETFs Are Eating Their Lunch

For decades, mutual funds were the go-to investment vehicle for Americans—offering diversification, professional management, and long-term growth. But a quiet revolution is underway. A 2024 Forbes report notes that passively managed assets have now overtaken active ones—and are expected to make up over 70% of the market within the next decade. The age of traditional mutual funds may be fading fast.

ETFs (exchange-traded funds) are increasingly beating mutual funds on cost, tax efficiency, and flexibility. Research from the University of Iowa shows that ETFs, on average, have lower expense ratios—around 0.21% compared to 0.45% for mutual funds. This doesn’t mean all mutual funds are bad—but many investors don’t realize the hidden costs they’re paying. And while that might sound harsh, once you dig into the fees, hidden taxes, and underwhelming returns, it seems that the system isn’t built to benefit individual investors—it’s built to collect fees.

Let’s break down why ETFs are dominating, how mutual funds quietly erode your returns, and what you should know before choosing either.

Key Takeaways

- Many mutual funds can charge higher fees and underperform benchmarks.

- ETFs can offer similar diversification but with lower costs and better tax efficiency.

- The shift from mutual funds to ETFs is accelerating.

- Investors should be aware of fees, tax drag, and performance consistency.

How Mutual Funds Work (And Some Problems)

Mutual funds pool money from many investors and invest in a basket of stocks or bonds, managed by a professional.

Sounds great, right? But here’s the catch:

1. Higher Fees

- Actively managed mutual funds often charge 0.75% to 1.5% in annual expenses.

- ETFs typically cost 0.03% to 0.25%.

That difference compounds. Over 30 years, it could cost you tens of thousands of dollars in lost returns.

2. Underperformance

SPIVA (S&P Dow Jones Indices) reports show that over 80% of active mutual funds underperform their benchmarks over 10 years.

3. Tax Inefficiencies

- Mutual funds distribute capital gains annually—even if you didn’t sell anything.

- ETFs use an “in-kind” redemption process to minimize capital gains.

The result? You may pay more taxes with mutual funds.

Why We Believe ETFs Are Taking Over

ETFs are structured to be lean, transparent, and efficient. They trade like stocks, meaning you can buy or sell anytime during market hours.

Common Advantages:

- Lower fees = More money stays in your pocket

- Lower tax impact = Fewer surprise capital gains

- Passive indexing = Often outperforms active mutual funds over time

- Transparency = You know exactly what you’re holding

The Marketing Machine of Mutual Funds

Mutual funds still dominate many 401(k) plans and retirement accounts. Why?

- Financial advisors may receive incentives to sell them.

- They’re legacy products baked into older retirement systems.

- The mutual fund industry spends billions on marketing.

But more investors are waking up—and reallocating to ETFs.

When Mutual Funds Might Still Make Sense

To be fair, there are a few cases where mutual funds may be worth it (in our opinion):

- Target-date retirement funds (some are structured only as mutual funds)

- Very specific active strategies with long-term outperformance (rare)

- Employer-sponsored plans where ETFs aren’t available

If you're paying a high fee, you'd better be getting consistent alpha—and that’s a big ask.