R.I.P 60/40 Portfolio?

In 2022, the traditional 60/40 portfolio—60% U.S. equities, 40% bonds—suffered a historic loss of over 16%, and the pain didn’t stop there. From the start of 2022 to mid-2024, it has entered what analysts call its worst stretch of underperformance in 150 years, according to a 2024 report covered by MSN. For many, this challenged a long-held belief: that bonds serve as a reliable hedge when stocks decline. But amid surging inflation and aggressive rate hikes, both sides of the portfolio fell together.

So where does that leave the 60/40 model in 2025? Is it outdated—or simply in need of recalibration?

This article explores how the strategy has evolved, where it faces limitations, and what adjustments investors are making in a more volatile market.

Key Takeaways

- The 60/40 allocation saw a historic loss in 2022, largely driven by inflation and rising interest rates.

- The strategy remains viable—but only when core assumptions around diversification and fixed income are reexamined.

- Investors are making updates, such as adding global assets, inflation hedges, or factor exposures.

- Investor behavior often outweighs allocation precision—consistency is key during drawdowns.

- Stress-testing tools and diversification metrics can provide insight into portfolio resilience in today’s environment.

What Went Wrong with the 60/40 Mix

The 60/40 structure has long been viewed as a balanced approach, offering growth from equities and stability from bonds. This trade-off held for years—particularly in low-inflation periods with falling interest rates.

But 2022 disrupted that balance. A World Economic Forum review showed the Federal Reserve raised rates from March through December 2022 at a pace unseen in over three decades—twice as fast as the 1988–89 tightening cycle. Inflation peaked above 9% (BLS, 2022), and bond values plunged, failing to cushion the simultaneous equity decline.

The result: both legs of the portfolio faltered.

This breakdown revealed the danger of correlation risk—when asset classes expected to move differently start falling in sync. If bonds and stocks drop together, a portfolio built on their inverse behavior may no longer offer real protection.

- Hypothetical Example: Picture a 38-year-old investor rebalancing into a 60/40 plan every quarter during 2022. With both assets declining, they’re effectively buying more of what’s falling—without the stabilizing effect of fixed income. Losses deepen, confidence erodes, and they may begin doubting the entire strategy.

For some, 2022 highlighted a core truth: historical models need to reflect today’s economic environment—not just long-term averages.

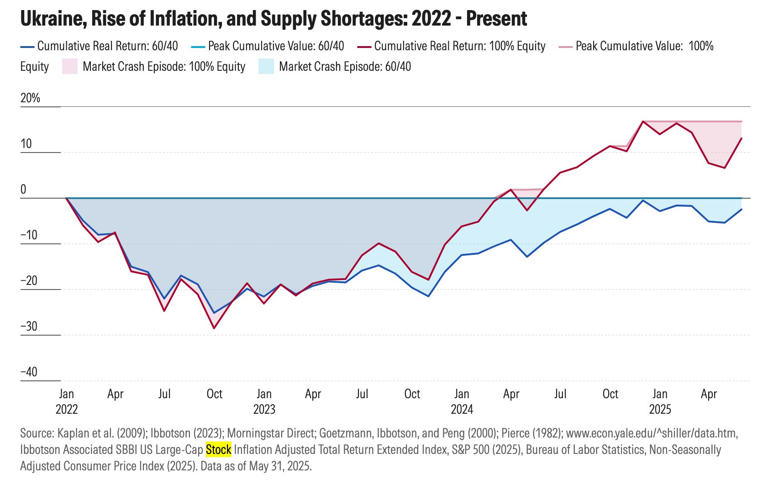

This chart shows that during 2022–2023, stocks and bonds declined in tandem—undermining the long-held belief that bonds reliably offset equity losses in diversified portfolios.

Reframing, Not Replacing

While the 60/40 model faced a significant challenge, it’s not necessarily obsolete. The key question isn’t whether it works—but under which market conditions it remains effective.

- In low-inflation, steady-rate settings, the mix may still deliver a workable balance of growth and downside protection.

- When inflation spikes or asset correlations shift, returns can deteriorate sharply.

As a result, many investors are tweaking—not abandoning—the approach. Some common adjustments include:

- Adding TIPS to help guard against real rate shocks

- Including commodities or tangible assets to provide inflation sensitivity

- Expanding into global markets to reduce U.S.-centric concentration

- Incorporating factor tilts, such as value or low volatility, to reshape return profiles

These changes don’t discard the 60/40 blueprint—they reinterpret its logic through a modern lens.

While recent losses have tested investors’ patience, history continues to reward diversified portfolios over the long haul. The chart below illustrates that both 60/40 and all-equity allocations have generated strong returns across decades of turbulence—from wars to inflation to recessions. Still, the recent gap in performance has sparked fresh debate over whether strategies rooted in the past still hold up in today’s environment.

Behavior Over Perfection

What often matters more than precise portfolio weights is the investor’s ability to stay committed. In volatile markets, emotional decisions—like panic-selling—can derail even the most sophisticated strategies.

A structure like 60/40, while simple, may be more effective for investors who benefit from clarity and repeatable rules. That makes behavioral compatibility a strategic asset.

In contrast, overengineering a portfolio—layering in complexity, trying to time cycles, or constantly rotating allocations—can invite risk and underperformance.

Said differently: the most effective strategy isn’t the most complex one. It’s the one an investor can actually stick with.

How to Pressure-Test Portfolio Assumptions

Today, many are shifting focus away from historical return averages and toward stress-testing portfolios under adverse scenarios. This approach may include:

- Diversification scoring: Quantifying how much asset classes actually move independently

- Drawdown simulations: Modeling past stress periods like 2008 or 2022

- Scenario planning: Estimating how inflation shocks or rate changes impact real returns

Rather than chasing an ideal allocation, this method evaluates how well a portfolio might hold up under strain.

Consistency in rebalancing—even within an imperfect structure—may be more important than chasing perfection.

FAQs

Q: Is the 60/40 portfolio obsolete after 2022?

A: Not necessarily. While it struggled during inflationary shocks, it may still perform well in more stable environments, especially with thoughtful modifications.

Q: What can replace the 40% bond component?

A: Depending on inflation and rate views, some investors rotate into TIPS, short-duration bonds, real assets, or select alternatives.

Q: Should younger investors avoid 60/40 entirely?

A: Not always. Younger individuals may favor more equity exposure but could still include bonds to moderate volatility. It comes down to risk tolerance and behavioral consistency.

Q: Is international diversification important?

A: Many include global assets to reduce U.S. concentration risk. That said, investors should also account for currency exposure and regional volatility.

Q: How often should a 60/40 strategy be rebalanced?

A: Some use fixed intervals like annual rebalancing, while others follow drift-based thresholds—adjusting only when allocations deviate by a set percentage.