The 2025 Tax-Saving Playbook: 25 Legitimate Strategies to Help You Keep More of What You Earn

25 IRS-compliant tax strategies to help you reduce your 2025 bill—tailored for different income levels, life stages, and goals. Note: this guide is not tax advice. Before making any decisions, speak with a qualified professional who can review your full financial picture.

According to IRS data through the week ending May 9, 2025, the average federal tax refund is $2,939—effectively the amount many households over-withheld through payroll deductions. This playbook shows you how to potentially reduce your tax liability and optimize your withholdings.

Inflation is squeezing budgets and markets are still volatile, but tax planning is one lever you fully control. Below are 25 tactics ordinary investors actually use, explained in plain English with “red-flag” caveats where DIY can backfire. Examine what fits, skip what doesn’t, and run anything complex past a qualified adviser.

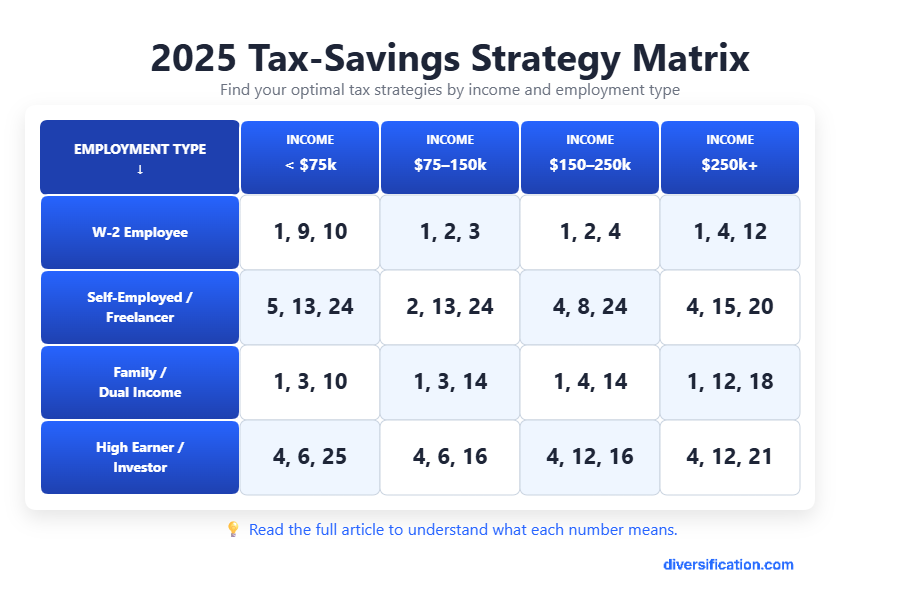

Quick-Select Guide

- Early-career employees → Strategies 1 · 3 · 10 · 25

- Self-employed / freelancers → Strategies 2 · 5 · 8 · 13 · 24

- Families / dual income → Strategies 3 · 4 · 9 · 14 · 18

- High earners / pre-retirees →Strategies 6 · 7 · 15 · 16 · 20 · 21

Need more precision? The matrix below filters by both income and life stage. Let’s start.

How much can you save on taxes? Get your audit here - Sign up to PortfolioPilot.com

1. Contribute to Tax-Advantaged Retirement Accounts

Traditional IRAs and 401(k)s can reduce your taxable income today. Roth IRAs don’t give an upfront deduction but offer tax-free growth and withdrawals later—often helpful in retirement when your tax bracket may be lower.

2025 Contribution Limits:

- Traditional & Roth IRA: $7,000 (or $8,000 if age 50+)

- 401(k)/403(b): $23,500 (or $31,000 if age 50+)

Hypothetical Example: You earn $90,000 and contribute $7,000 to a Traditional IRA. That reduces your taxable income to $83,000. Assuming you're in the 18% marginal federal tax bracket, you’d save $1,260 in federal taxes.

Note: Contribution limits are updated annually. Always confirm current numbers with the IRS.

Want to compare Traditional vs. Roth IRA in more depth?

Check out this IRS page.

2. Max Out Your HSA Contributions

Health Savings Accounts (HSAs) offer triple tax advantages:

- Contributions are tax-deductible (even if you don’t itemize)

- Growth is tax-free

- Withdrawals for qualified medical expenses are also tax-free

Eligibility: You must be covered by a high-deductible health plan (HDHP) to contribute.

2025 Contribution Limits:

- $4,300 for self-only coverage

- $8,550 for family coverage

- Additional $1,000 catch-up contribution if age 55+

Hypothetical Example: You’re 35, have family HDHP coverage, and contribute the full $8,550 to your HSA. That amount reduces your taxable income by $8,550. If you’re in the 22% federal tax bracket, that means a federal tax savings of approximately $1,881.

You use $3,000 for qualified expenses tax-free, and the remaining $5,550 stays invested and grows without tax drag.

Want to learn how HSA investing works or what expenses qualify?

Check out IRS Publication 969.

3. Use FSAs for Health and Dependent Care

Flexible Spending Accounts (FSAs) let you pay for qualified medical and dependent care expenses using pre-tax dollars, lowering your taxable income.

- Healthcare FSA: $3,300

- Dependent Care FSA: $6,600 (if married filing jointly)

Hypothetical Example: You elect to contribute the full $3,300 to a Healthcare FSA in 2025 and use it for planned dental and vision expenses. If you're in the 24% federal tax bracket, that pre-tax contribution saves you approximately $792 in federal income taxes.

Key Considerations: FSAs are generally “use it or lose it” accounts. Any unused funds may be forfeited at year-end (though some plans offer grace periods or limited carryovers). Make sure to plan contributions around expected expenses.

4. Harvest Tax Losses

If you hold investments in taxable brokerage accounts that have declined in value, you may be able to sell them at a loss to offset realized capital gains—or up to $3,000 of ordinary income per year. This strategy, known as tax-loss harvesting, can lower your total tax bill if done correctly.

- Hypothetical Example: You sold Stock A earlier in the year for a $5,000 gain. Later, Stock B declines in value, and you sell it for a $5,000 loss. These two transactions cancel each other out, eliminating any capital gains tax liability for the year. Assuming you’re in the 24% capital gains bracket, this maneuver saves you $1,200 in taxes.

- Important: The wash-sale rule disallows the deduction if you buy a substantially identical asset within 30 days.

- Note: Selling a losing investment and then buying it back within that window—before or after—will likely violate the rule, disqualifying the loss for tax purposes. Make sure you’re not accidentally resetting the clock - Read more about it in our full article: The Wash Sale Rule.

In practice, tax-loss harvesting can meaningfully reduce your tax bill—if done correctly. In 2024 alone, users of the PortfolioPilot.com tax optimization feature saved over $11 million through tax-loss harvesting, based on an internal analysis of activity across 24,000 users as of November 18, 2024¹. Curious how this could apply to your portfolio? Try the tax optimization tool.

5. Delay Income Strategically

Deferring income to the next tax year can reduce your current year’s taxable income—especially if you expect to be in a lower bracket next year. This strategy is most effective when paired with careful cash flow planning.

- Who It Applies To: Freelancers, consultants, small business owners.

- Hypothetical Example: You’re a freelancer earning $90,000 in 2025 and expect to earn $60,000 in 2026. By delaying a $10,000 invoice from December to January, your 2025 taxable income drops to $80,000. Assuming you’re in the 24% federal tax bracket, this move reduces your 2025 tax bill by approximately $2,400.

- Key Considerations: Ensure you aren’t compromising cash flow and be mindful of potential estimated tax adjustments.

To learn more: IRS Publication 334

6. Convert to a Roth IRA During Low-Income Years

Roth conversions can be powerful when your income dips temporarily. You pay taxes now to enjoy tax-free withdrawals later—especially useful during career breaks or early retirement.

- Who It Applies To: Individuals in temporarily lower tax brackets or early retirees.

- Hypothetical Example: You retire at 58, have no earned income this year, and convert $30,000 from your Traditional IRA to a Roth. You claim the standard deduction ($14,600 for single filers in 2025), which lowers your taxable income to $15,400. This puts most of the conversion in the 12% tax bracket, resulting in approximately $1,848 in taxes now.

If you had waited and withdrawn the $30,000 during retirement in the 22% bracket, you’d pay $6,600 in taxes instead—meaning this timely Roth conversion saves you around $4,750 in long-term taxes, while locking in future tax-free growth.

- Key Considerations: This increases your taxable income in the year of conversion. Model scenarios beforehand.

To learn more: IRS Roth IRA Conversion Rules

7. Deduct Mortgage Interest (If You Itemize)

Mortgage interest on loans up to $750,000 is deductible if you itemize—and it can be one of the largest deductions available to homeowners.

- Who It Applies To: Homeowners with qualifying mortgages.

- Hypothetical Example: You paid $12,000 in mortgage interest in 2025. If you itemize and are in the 24% tax bracket, that deduction lowers your tax bill by $2,880.

- Key Considerations: Compare against the standard deduction—itemizing only makes sense if total deductions exceed it.

To learn more: IRS Topic 505 – Interest Expense

8. Use the Home Office Deduction (if self-employed)

If you're self-employed and work from home, a portion of your housing expenses may be deductible—including rent, utilities, and insurance.

- Who It Applies To: Freelancers, independent contractors, business owners.

- Hypothetical Example: Your home office is 10% of your home’s square footage. You pay $15,000 annually in qualified housing expenses. You can deduct $1,500.

- Key Considerations: Must be a regular and exclusive workspace. Not available to W-2 employees.

To learn more: IRS Home Office Deduction

9. Claim Education Credits

The American Opportunity Credit and Lifetime Learning Credit can reduce your tax bill directly when paying for qualified higher education expenses.

- Who It Applies To: Students and parents paying post-secondary education expenses.

- Hypothetical Example: You pay $4,000 in college tuition. The American Opportunity Credit covers 100% of the first $2,000 and 25% of the next $2,000—totaling $2,500.

- Key Considerations: Income phaseouts apply, and credits can’t be claimed for the same student by multiple taxpayers.

To learn more: IRS Education Credits

10. Explore the Saver’s Credit

This little-known credit rewards low- to moderate-income earners for saving for retirement. It's a dollar-for-dollar reduction in your tax bill—on top of the deduction or tax-free growth you may already get.

- Who It Applies To: Individuals with adjusted gross income below set IRS thresholds.

- Hypothetical Example: You contribute $2,000 to a Roth IRA and qualify for a 20% Saver’s Credit. That’s a $400 reduction in your tax bill. In this scenario, you would save $400 in taxes.

- Key Considerations: The credit is non-refundable and phases out at higher income levels.

To learn more: IRS Saver’s Credit Information

11. Track Charitable Contributions Properly

If you itemize, donations to qualified charities can reduce your taxable income. But documentation matters—especially if audited.

- Who It Applies To: Taxpayers who itemize and give to recognized nonprofits.

- Hypothetical Example: You donate $5,000 to a 501(c)(3) charity. At a 24% tax rate, that deduction lowers your tax bill by approximately $1,200.

- Key Considerations: Keep official receipts and acknowledgment letters. Contributions must be made before year-end.

To learn more: IRS Charitable Contributions Guidelines

12. Donate Appreciated Assets

Giving stock instead of cash can help you avoid capital gains taxes and still deduct the full market value—making your donation go further.

- Who It Applies To: Investors with appreciated assets held over one year.

- Hypothetical Example: You donate $10,000 in appreciated stock that you originally purchased for $5,000. You avoid paying capital gains tax on the $5,000 gain—which, at a 20% capital gains rate, saves you $1,000 in taxes. You also get to deduct the full $10,000, which—at a 24% income tax rate—lowers your tax bill by $2,400. In total, you save $3,400 in taxes by donating stock instead of cash.

- Key Considerations: Must donate to a qualified charity. Confirm the asset's holding period and value.

13. Qualify for the QBI Deduction (Section 199A)

Pass-through business owners may be eligible to deduct up to 20% of their qualified business income—one of the biggest tax benefits for entrepreneurs.

- Who It Applies To: Sole proprietors, partnerships, LLCs, S corps.

- Hypothetical Example: Your freelance business earns $80,000. You qualify for a $16,000 deduction. At a 24% tax rate, that saves $3,840.

- Key Considerations: There are income limits and phaseouts. Some business types may be excluded.

To learn more: IRS QBI Deduction Overview

14. Leverage 529 Plans for Education

529 savings plans grow tax-free, and withdrawals for qualified education expenses are also tax-free—making them a powerful tool for college planning.

- Who It Applies To: Parents, grandparents, and students saving for future education costs.

- Hypothetical Example: You invest $40,000 in a 529 plan for your child’s future college expenses. Over time, it grows to $60,000. When you use the full amount for qualified tuition, you avoid paying taxes on $20,000 in capital gains. At a 15% long-term capital gains rate, that’s $3,000 in tax savings.

- Key Considerations: Some states offer deductions or credits on contributions.

To learn more: 529 Plan

15. Consider a Donor-Advised Fund (DAF)

A Donor-Advised Fund lets you make a large charitable contribution in one year, take the full deduction up front, and distribute the money to charities gradually over time.

- Who It Applies To: Donors who want to bunch donations or give strategically.

- Hypothetical Example: You contribute $25,000 in appreciated stock to a DAF in 2025. You originally purchased the stock for $15,000, meaning there's a $10,000 capital gain.

- By donating the stock instead of selling it, you avoid $2,000 in capital gains tax (20% of $10,000) and also claim a $25,000 income tax deduction, saving $6,000 (24% of $25,000). In total, you save $8,000 in taxes—while giving the full $25,000 to causes you care about over time.

- Key Considerations: Once donated, funds are irrevocable. Plan ahead if timing deductions around income years or market gains.

16. Know When to Realize Capital Gains

Holding investments longer than 12 months qualifies you for lower long-term capital gains tax rates. Timing sales with lower income years can further boost tax efficiency.

- Who It Applies To: Investors in taxable brokerage accounts.

- Hypothetical Example: You sell a stock after holding it for 13 months and realize a $10,000 gain. Because you qualify for the 15% long-term capital gains rate, your tax bill is $1,500. If you had sold the same stock after only 11 months, the gain would be taxed as ordinary income. Assuming a 24% tax bracket, you'd owe $2,400 in taxes. In this scenario, holding the asset for just two more months saves you $900 in taxes.

- Key Considerations: Monitor both holding periods and your overall income for timing gains wisely.

To learn more: IRS Topic No. 409 Capital Gains and Losses

17. Gift Strategically Within Annual Limits

Gifting can reduce your taxable estate while helping family or others today. The IRS lets you gift up to $19,000 per recipient (in 2025) without using your lifetime exemption or filing extra forms.

- Who It Applies To: Individuals doing estate or wealth transfer planning.

- Hypothetical Example: You gift $19,000 each to two adult children. That’s $38,000 removed from your estate tax-free. At a hypothetical 40% estate tax, you reduce potential future tax liability by $15,200.

- Key Considerations: Gifts over the annual limit must be reported. Track lifetime exemption if planning large transfers.

To learn more: IRS Gift Tax FAQs

18. Bunch Itemized Deductions

If you don’t exceed the standard deduction most years, you can “bunch” charitable gifts or medical expenses into one year to itemize and maximize tax savings.

- Who It Applies To: Taxpayers near the standard deduction threshold.

- Hypothetical Example: You normally donate $10,000 per year. If you donate $20,000 in 2025 and nothing in 2026, you itemize in 2025 and take the standard deduction in 2026. At a 24% rate, you get $4,800 in tax savings from the 2025 donation.

- Key Considerations: Align timing with other deductions like mortgage interest and medical bills.

To learn more: IRS Publication 529 - Miscellaneous Deductions

19. Use State-Specific Tax Credits

Many states offer their own tax credits for education, energy-efficient upgrades, caregiving, or charitable contributions. These can be more generous than federal deductions.

- Who It Applies To: Residents of states with targeted incentives.

- Hypothetical Example: A Colorado resident donates $1,000 to a qualifying child care program and receives a 50% state tax credit. That’s $500 directly off their Colorado state tax bill.

- Key Considerations: Credit programs vary widely by state. Check local rules and filing procedures.

20. Understand the AMT and Plan Accordingly

The Alternative Minimum Tax (AMT) recalculates your tax bill using different rules—ignoring some deductions and exemptions. If you exercise incentive stock options or have high state tax deductions, you might trigger it.

- Who It Applies To: High earners or those with large itemized deductions.

- Hypothetical Example: You exercise $100,000 worth of incentive stock options and itemize $40,000 in deductions. Due to AMT, your final tax bill rises by $7,000 compared to the standard method. With planning—such as exercising fewer shares or spreading across years—you could have cut that extra liability in half. In this scenario, you would save $3,500 in taxes.

- Key Considerations: Run projections ahead of time—AMT is a common trap for tech employees and those with large deductions.

To learn more: IRS Form 6251 and AMT Overview

21. Invest in Municipal Bonds

Municipal bonds (“munis”) are often exempt from federal—and sometimes state—income taxes. For investors in high tax brackets, they can yield more after-tax than higher-yielding taxable bonds.

- Who It Applies To: High-income investors focused on tax-efficient income.

- Hypothetical Example: You invest $100,000 in a muni bond paying 4%. In a 35% federal bracket, that’s equivalent to earning over 6% in a taxable bond. Compared to a 5% corporate bond, you’d net $3,250 vs. $3,000 after tax.

- Key Considerations: Not all muni bonds are AMT-exempt. Review state tax treatment too.

22. Time Your Required Minimum Distributions (RMDs)

Starting at age 73 (or 75 if born in 1960+), retirees must begin taking RMDs from traditional retirement accounts—or face steep penalties.

- Who It Applies To: Retirees with Traditional IRAs or 401(k)s.

- Hypothetical Example: You have $800,000 in a Traditional IRA. Your first RMD is $30,000. If you skip it, you could owe a penalty of 25%, or $7,500. By planning ahead, you take the RMD, spread it over quarters, and stay in a lower bracket—reducing the tax hit from $7,500 to $5,100.

- Key Considerations: Missing an RMD now carries a lower penalty than in the past—but it's still costly.

To learn more: IRS RMD FAQs

23. Explore the Backdoor Roth Strategy

High earners who exceed Roth IRA income limits can still contribute using a workaround: contribute to a non-deductible Traditional IRA, then convert it to Roth.

- Who It Applies To: Individuals above Roth income limits.

- Hypothetical Example: You earn $220,000, so you can’t directly contribute to a Roth IRA. Instead, you contribute $7,000 to a non-deductible Traditional IRA, then convert it to a Roth the following week. If you have no other pre-tax IRAs, the entire amount is tax-free. Over 30 years, that $7,000 could grow to $53,000 tax-free, assuming a 7% average annual return—a typical long-term estimate for diversified stock portfolios. If this growth were taxed at a 20% capital gains rate in a taxable account, you’d owe around $9,200 in taxes. By using a Roth conversion, you avoid that future tax bill entirely.

- Key Considerations: Watch the pro-rata rule—existing pre-tax IRA balances complicate the math.

To learn more: Backdoor Roth IRA: White Coat Investor Guide

24. Deduct Self-Employed Business Expenses

Freelancers and business owners can deduct ordinary and necessary expenses—including software, internet, office supplies, and part of their home if used exclusively for work.

- Who It Applies To: Self-employed individuals, freelancers, contractors.

- Hypothetical Example: You spend $3,000 on business tools, web hosting, and marketing. If you’re in a 24% tax bracket, you reduce your tax liability by $720.

- Key Considerations: Keep clean records and separate personal vs. business use. Over-deducting can raise audit risk.

To learn more: IRS Self-Employed Tax Center

25. Keep Meticulous Records

Clean documentation protects your deductions and simplifies filing. You don’t need to go full forensic accountant—but save receipts, log mileage, and use digital tools where possible.

- Who It Applies To: Everyone.

- Hypothetical Example: You use a digital app to track $6,000 in charitable donations, medical bills, and business expenses throughout the year. If audited, your full deduction is allowed. At a 22% rate, that’s $1,320 you keep.

- Key Considerations: Retain records for at least three years. Cloud-based tools make it easier than ever.

To learn more: IRS Recordkeeping for Individuals

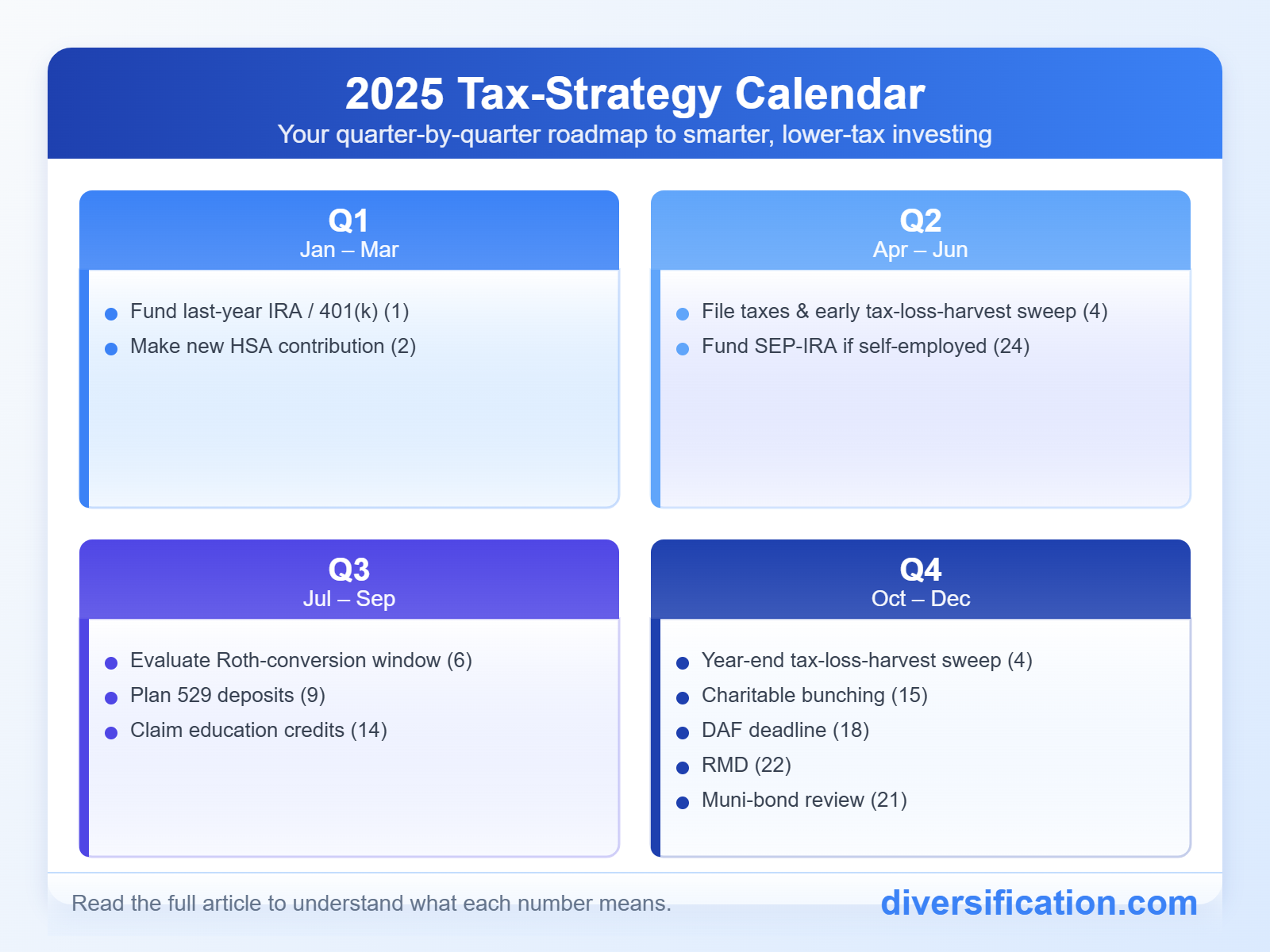

Stay Ahead with Quarterly Tax Checkups

Tax planning isn’t just for year-end. Many of these strategies are most powerful when used early and reviewed regularly. Even small tweaks—like adjusting a paycheck contribution or planning a charitable gift before year-end—can make a meaningful difference.

To help guide your timing, here’s a simple quarter-by-quarter roadmap for applying these strategies throughout the year:

You likely don’t need to apply all 25 strategies. But understanding which ones might apply to you is a big step forward.

And remember: this guide is not tax advice. Before making any decisions, speak with a qualified professional who can review your full financial picture.

¹. The estimated tax savings referenced are based on aggregated, unaudited internal data and reflect potential opportunities, not actual realized outcomes. These figures are not guarantees of results and do not account for individual tax circumstances, execution timing, or other factors that may materially affect outcomes. PortfolioPilot does not provide personalized tax advice. Users should consult a qualified tax professional before acting on any tax-related strategies.