june 10, 2025

4

min read

💬 Daily Observation

“The biggest investing errors come not from factors that are informational or analytical, but from those that are psychological.” – Howard Marks, The Most Important Thing Illuminated: Uncommon Sense for the Thoughtful Investor.

I remembered this amazing book from Howard Marks that I first read in college and still find gold, which highlights that even perfect data or models can’t save us if emotions hijack our decisions. When markets rally, it’s natural to feel excitement, yet chasing momentum can lead to buying high and regretting later. In downturns, fear tempts us to sell at lows, but pausing to ask “Is this reaction rooted in fundamentals or panic?” can prevent costly mistakes. For busy investors juggling work, family, and multiple accounts, it’s easy to be swept up by headlines or social-media chatter. Instead, cultivating self-awareness—recognizing when anxiety or overconfidence arises—allows you to slow down and stick to your plan.

Over time, practicing this discipline builds confidence in your convictions and reduces regret from impulsive trades. Remember, investing is a human endeavor: understanding your own psychology can be the edge that transforms market volatility from a threat into an opportunity for thoughtful action.

Next time you feel the tug of FOMO or fear, take a breath and stick to your plan—it could be the edge that steadies your journey.

☕ So grab your coffee, and let’s dive in today's fresh edition of Diversification Daily.

🗞️ Today's stories that matter (and why)

1. 📉 Fed expected to hold rates through September

The US Federal Reserve is widely anticipated to maintain its policy rate at 4.25%–4.50% at the upcoming June meeting and hold through at least September amid persistent inflation risks and uncertain trade dynamics.

Economists point to sticky price pressures partly driven by tariff policies and elevated federal deficits as reasons for caution. A recent New York Fed survey showed easing one-year inflation expectations but still above target, reinforcing the Fed’s data-dependent yet cautious stance.

While some foresee rate cuts later in the year, the Fed’s priority remains ensuring inflation sustainably trends toward 2% before easing monetary policy.

Why it matters: A prolonged high-rate environment may support cash-like instruments but could weigh on interest-rate-sensitive sectors, necessitating a balanced portfolio approach between income and growth assets.

Assets in focus: Fixed Income

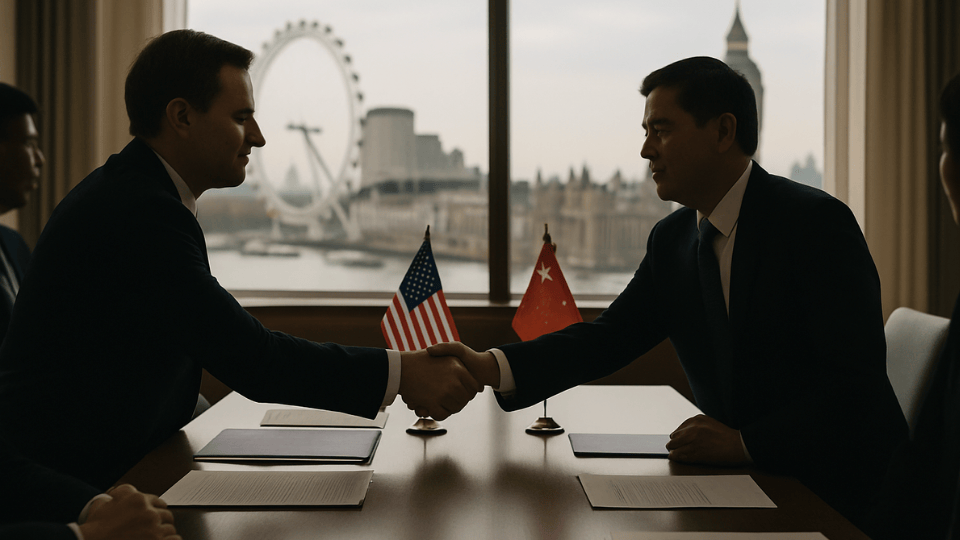

2. 🤝 US–China trade talks continue in London

Top US and Chinese officials met for a second day of negotiations in London, focusing on export controls, rare-earth materials, and tariff rollbacks, following a preliminary deal in Geneva. Participants include key figures such as the US Treasury Secretary and Chinese Vice Premier, reflecting the high stakes in resolving supply-chain disruptions for semiconductors and strategic industries. Despite positive rhetoric, no immediate comprehensive agreement is expected; markets are watching for limited concessions, like temporary rare-earth export licenses for US automakers, which could ease critical bottlenecks. The talks come amid steep declines in China’s exports to the US and broader concerns about global trade fragmentation.

Why it matters: Even small advances in US–China talks, can ease supply-chain strains and benefit cyclical industries like semiconductors and autos. However, without a comprehensive agreement, uncertainty and bouts of volatility are likely to persist.

Assets in focus: Equities

3. 🌍 World Bank lowers global growth forecast

The World Bank has lowered its 2025 global growth projection from 2.7% to 2.3%, citing escalating trade tensions—especially US tariffs—and weaker investment and trade flows. Advanced economies, including the US, face reduced growth forecasts (US outlook cut to around 1.4%), while emerging markets contend with sluggish domestic demand and policy uncertainties.

Inflation is expected near 2.9%, posing challenges for central banks balancing growth and price stability. The report highlights risks of prolonged stagnation and underscores the need for coordinated trade negotiations and technological collaboration to boost prospects.

Why it matters: With slower global growth, investors should evaluate portfolio exposure to cyclical assets, consider defensive positioning, and stay alert to policy shifts that could alter growth trajectories or market sentiment.

Assets in focus: Equities

4. 🛍️ China's deflation deepens amid property crisis

China is experiencing deepening deflation, with consumer prices falling as wages and property values decline amid overcapacity and weak demand. Households increasingly turn to second-hand markets for discretionary items, with luxury goods available at steep discounts, signalling broader consumer caution. Businesses engage in aggressive price wars, risking unsustainable margins and potential closures, which may exacerbate job losses and further depress spending. Policymakers face pressure to deploy stimulus but must navigate debt concerns and ensure targeted support without inflaming financial risks.

Why it matters: Deflationary pressures in the world’s second-largest economy can weigh on global growth, commodity demand, and supply chains.

Assets in focus: Equities

5. 🏠 Real Estate investors increase home selling activity

A Realtor® report shows investors accounted for 10.8% of home sellers in 2024, the highest investor seller share ever recorded. Small investors led purchases but the gap between buying and selling narrowed to the smallest margin in five years, indicating many are rebalancing portfolios.

Cash purchases by investors fell to their lowest level since 2008, with greater reliance on debt financing evident. Geographic data indicate markets such as California and Minnesota saw net-positive investor selling, contributing to modest inventory improvements for typical homebuyers.

This trend may temper price growth and influence mortgage origination volumes as supply dynamics shift.

Why it matters: Shifts in investor selling affect housing supply-demand balances, with implications for home price trajectories, mortgage-backed securities spreads, and valuations of housing-related equities such as homebuilders and REITs.. Diversified portfolios with real estate exposures should account for evolving inventory conditions and potential regional divergences when calibrating allocations in housing-sensitive asset classes.

Assets in focus: Real Estate

🌀 Diversification Score – Have you evaluated your portfolio's diversification?

Are you spread across the right risk factors—or leaning on just a few big bets?

📊 Market Movements Snapshot

Asset Classes:

- 🟢 Emerging Markets Equities: +9.47 YTD. Emerging markets have rallied around 9.5% YTD as a softer dollar, prospects for Chinese stimulus, and stronger regional fundamentals in Latin America and Asia have attracted yield-seeking flows.

- 🟢 Real Estate: +2.46% YTD. Real estate (REITs) has posted modest gains as easing bond yields improve cap-rate spreads, supply constraints support rents, and occupancy trends stabilize despite lingering financing cost headwinds.

For the full list, click here

Sectors:

- 🟢 Utilities: +7.66% YTD. Utilities have outperformed as yield-hunting investors price in expected Fed rate cuts, valuing stable dividends, and supportive infrastructure/clean-energy investment themes bolster sector resilience.

- 🔴 Energy: −1.84% YTD. Energy trails as oil prices remain range-bound amid mixed supply-demand signals and transition-related pressures, with OPEC production adjustments offsetting demand moderation and weighing on sentiment.

For the full list, click here

🤯 Alternative investment highlight: 🛍️ China’s second-hand luxury market sees extreme discounts amid deflation

China’s prolonged deflation—driven by a persistent property-sector downturn and overcapacity—has led to deeply discounted second-hand luxury goods, with designer handbags, watches, and accessories trading at up to 90% off original prices.

Platforms like Super Zhuanzhuan and DeWu are expanding rapidly to handle the oversupply, but shrinking buyer power and rising authentication costs threaten many new entrants. Millennials and Gen Z are driving resale demand for cost savings and sustainability, even as China’s broader luxury market fell an estimated 18–20% in 2024 and is expected to stay flat in 2025.

This surge in supply creates margin pressure that mirrors distressed repricing cycles in other asset classes, offering alternative investors vivid lessons on value dynamics and platform viability under stress.

🧠 From the Education Center: Diversification, a Practical Guide

Diversification is powerful—but only when it’s done right. Learn how to spread risk smartly across assets, geographies, and time.

📤

Share with a Friend

Forward this email if Diversification Daily keeps your investing compass steady.

🚨 Your $1,000 Question—Answered

What should you do with your next $1,000?

PortfolioPilot analyzes your full financial picture and tells you exactly where that money may work hardest. Whether it's optimizing taxes, rebalancing your risk, or investing idle cash—it delivers smart, personalized answers.

Put your money to work → PortfolioPilot.com

Feel free to reply to this email with any questions or feedback.

See you tomorrow,

Fernanda de Francesco,

Editor, Diversification.com

©2025 diversification.com.

IMPORTANT DISCLOSURES: diversification.com is a technology product of Global Predictions Inc, a Registered Investment Advisor with the SEC. The information provided on diversification.com is for informational and educational purposes only. It should not be considered financial advice. Investment advisory services are only provided to investors who become Global Predictions clients. Past performance is not a guarantee of future results. Investing involves risk.

The content on this website, including market analysis, diversification scores, and other information, represents our observations of current market conditions and should not be interpreted as a recommendation to buy, sell, or hold any particular investment or security.

Past performance is not indicative of future results. All investments involve risk, including the possible loss of principal. Diversification does not guarantee a profit or protect against a loss in a declining market.

The diversification score and related analysis are based on a proprietary methodology that evaluates various aspects of portfolio composition. They should not be the sole basis for making investment decisions.

DATA SOURCES: Market data, asset class information, sector analysis, and other financial information displayed on this website are sourced from StockNewsAPI, Morningstar, AlphaVantage, IEX, and TradingEconomics. We make every effort to ensure data accuracy but cannot guarantee that all information is complete, accurate, or timely.

USER COUNT DISCLOSURE: References to "30,000 users/subscribers" reflect the combined user base across Global Predictions, PortfolioPilot.com, and diversification.com platforms as of February 15, 2025.

REGULATORY INFORMATION: For Global Predictions' Form ADV Part 2A and other regulatory disclosures, please visit portfoliopilot.com/disclosures.

FIDUCIARY ADVICE: Fiduciary financial advice is available through PortfolioPilot.com. The tools and calculators on diversification.com are for educational purposes and do not constitute personalized investment advice.

Before making any investment decisions, you should consult with a qualified financial advisor, tax professional, or legal counsel to ensure that your investment strategy aligns with your individual needs and circumstances.

Global Predictions Inc. and its affiliates, officers, directors, employees, and agents do not guarantee the accuracy, completeness, or timeliness of the information provided on this website and shall not be liable for any losses, damages, or costs that may arise from its use.

*For compliance reasons, these stories are complete fiction with made up characters and portfolios. Possibly influenced by real interactions, and definitely not financial advice."